Table of Content

If you use your home equity loan to complete home renovations or improvements, the interest is tax-deductible. Plus, if you use your home equity loan for property improvements, you may be simultaneously increasing the value of your property while being able to enjoy the investment in your space while you live there. Alix is a staff writer for CNET Money where she focuses on real estate, housing and the mortgage industry. She previously reported on retirement and investing for Money.com and was a staff writer at Time magazine. She has written for various publications, such as Fortune, InStyle and Travel + Leisure, and she also worked in social media and digital production at NBC Nightly News with Lester Holt and NY1. She graduated from the Craig Newmark Graduate School of Journalism at CUNY and Villanova University.

Discover Home Loans pays all closing costs incurred during the loan process, so that you don’t have to bring any cash to your loan closing. Home equity loans are popular among borrowers who want to use the funds to cover large expenses, such as home improvement projects or high-interest debt consolidation. Connexus has the fastest closing timelines among the lenders we surveyed, with about 25 days to close. It also has a lower required credit score and a higher CLTV than some lenders. The rate quoted above is good for a 10-year loan term, though you can borrow for terms of five to 30 years.

The Person-trade-off Approach to Valuing Health Care Programs

Joining is easy and comes not only with a wide variety of money-saving products tailored to fit your needs, but also exclusive member-only benefits. Top Considerations For Buying A New Construction Home Are you ready to make a big move? See if building a new home is something you should consider based on these benefits and drawbacks. The first parameter will allow you to borrow up to 80% of the Fair Market Value of the home, less any liens you may already have on the home.

While, with a variable interest rate, your interest rate and payment can change over time due to a variety of factors. The APR that Fifth Third advertises is offered to borrowers with the highest credit scores and qualifications. The lowest rate also includes a 0.25% discount for borrowers who set up automatic payments from an eligible Fifth Third account. Discover makes its home equity loans available to borrowers with the lowest credit scores among the national lenders surveyed. The interest rate is slightly higher than some competitors, however. How To Negotiate Your Bills & Debts Learn how to ask for discounts and modifications in order to better afford your monthly payments.

You’re signed out

We are providing the link to this website for your convenience, or because we have a relationship with the third party. Discover Bank does not provide the products and services on the website. Please review the applicable privacy and security policies and terms and conditions for the website you are visiting. Discover Bank does not guarantee the accuracy of any financial tools that may be available on the website or their applicability to your circumstances. For personal advice regarding your financial situation, please consult with a financial advisor.

There are a few options available if you’re looking to use your home’s equity. These include a Home Equity Loan, a Home Equity Line of Credit, and a Cash-Out Refinance. Home equity is a valuable asset that can be used to reach a variety of financial goals. A+FCU helps to make sure you understand the ins and outs of home equity loans and compare your options. Home equity loans use your home as security, so their rates are often lower than other forms of borrowing. Ryan Eichler holds a B.S.B.A with a concentration in Finance from Boston University.

Senior Investment Manager Equity

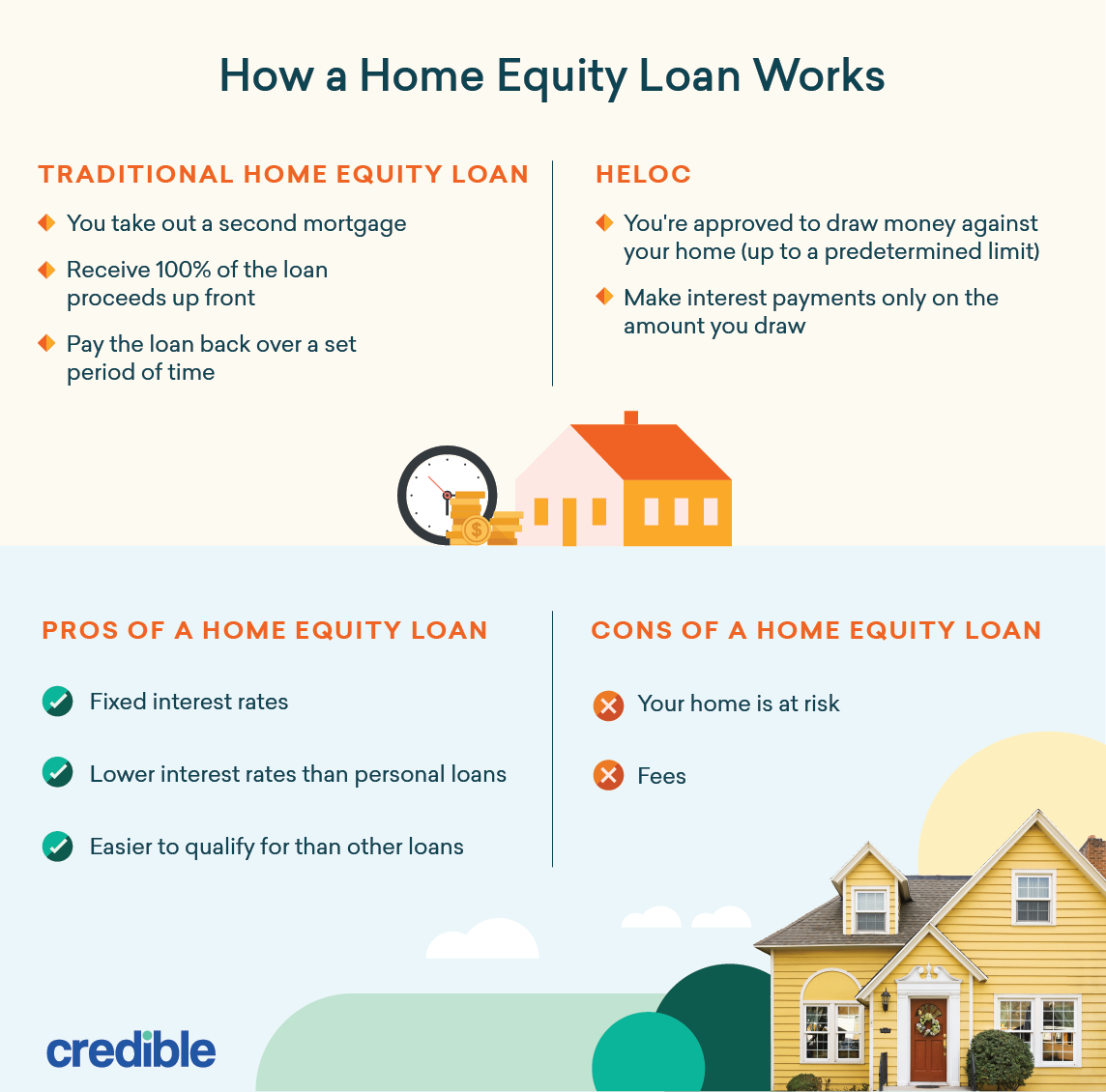

A HELOC, or home equity line of credit, allows you to leverage the equity you’ve built in your home to get cash for home improvements or other expenses. Unlike a home equity loan, you don’t have to get a lump sum payment at closing. Instead, your lender extends you a line of credit that you can draw from as needed over a specified period. In this way, you can get just the money you need, as you need it.

As you pay down the HELOC over time, you can get more money at any point during the draw period . Home equity offerings vary, so reviewing the terms and conditions applicable to the product you’re considering is important. The information in this article is provided to help you better understand these options and may not reflect products or offerings available from AmeriSave. If you want to do more research before you hit "apply," you have options, too.

Customer service

A home equity loan generally comes with a lower interest rate than other types of loan products since your home serves as collateral for the loan. If you have outstanding debt on a credit card, a personal loan, student loans or other debts, consolidating with a home equity loan could make it cheaper to pay off those debts. A home equity loan allows you to convert a portion of the equity you’ve built in your home to cash. It’s also an effective way to consolidate debt and eliminate high-interest credit card and loan balances sooner. That’s because the average interest rate on home equity loans is often lower than that of a credit card. HELOCs typically have variable interest rates, meaning the monthly payment could fluctuate over time.

Some smaller lenders cap home equity loans at $250,000, but others offer loans of up to $500,000. In addition, most lenders have a minimum threshold of $10,000 to open a home equity loan. The amount you can borrow depends on the equity you have in your home. Most lenders prefer borrowers to have at least 20% equity before they'll issue a loan. Most also limit their loans to no more than 80% of your equity. If you're a homeowner, you may be sitting on a golden egg—your home's equity.

Marc is senior editor at CNET Money, overseeing banking and home equity coverage. He's been a financial writer and editor for more than two decades, working for The Kiplinger Washington Editors, U.S. News & World Report, Bankrate and Dow Jones. Before joining CNET Money, Wojno was Senior Editor of Finance for ZDNet, writing on blockchain, cryptocurrency, financial services, investing and taxes.

The Fed doesn't directly control fixed mortgage rates, however — the most pertinent number is the 10-year Treasury yield. Even so, high inflation all but forces the Fed to act aggressively, and it sets the tone for rates overall. As price inflation persists, the Federal Reserve again moved aggressively at its November meeting. The Federal Reserve raised rates three-quarters of a percentage point for the fourth consecutive meeting, a strong policy move that continues to translate to rising mortgage rates. "The refinance of our house was fast and simple. The overall process was very simple, easy, and best of all, Mackenzie got us a great rate. Dropping our interest rate by almost 2%. Prosper help center Answers to home equity questions, from your application to payments.

Fortunately, Lower offers prequalification, which means that you can see if you’re eligible for a loan without a hard credit check. Because these fees can vary based on your situation and where you live, be sure to speak with the lender before accepting the loan to make sure you understand what costs you’ll be responsible for. Lower charges an origination fee of 1 percent and a $495 application fee for home equity loans and HELOCs. There are no annual fees, though you may still be on the hook for other fees, such as title and appraisal fees.

It does help you save in the long term, but with less time to pay, 15-year mortgages have higher monthly payments. Like regular mortgages, home equity loans have closing costs, such as origination fees, recording fees, and appraisal fees. To do a fair, apples-to-apples comparison of the rates charged by different lenders, you'll want to focus on each loan's annual percentage rate . In addition to the loan's basic interest rate, the APR takes some of the loan fees into account, giving you a more accurate picture of what you'd really be paying to borrow.

Agents Nationwide

For example, if you're planning to move soon, a home equity loan probably won't make financial sense; without your home to secure the loan, you are responsible for paying back the balance of your loan to your lender. "Until inflation peaks, mortgage rates won't either," says Greg McBride, CFA, Bankrate chief financial analyst. At the current average rate, you'll pay $632.73 per month in principal and interest for every $100,000 you borrow. The majority of closely watched refinance interest rates tapered off today versus this time last week, according to data compiled by Bankrate. "The ongoing moderation in home-price growth, along with further declines in mortgage rates, may encourage more buyers to return to the market in the coming months," Joel Kan, an MBA economist, wrote in a release.

Outside the digital world, Marc can be found spinning vinyl, threading reel-to-reel tapes, shooting film with his Bolex and hosting an occasional pub quiz. If you aren’t sure how much money you need, a home equity line of credit may be a better choice for you. They are revolving forms of credit, so you can tap into them again and again during the draw period. Instead, using a home equity loan—and leaving your existing mortgage in its current state—may lower your overall repayment cost. Our experts have been helping you master your money for over four decades.

No comments:

Post a Comment